Peace in our time?

Despite optimistic talk, here I affirm my cautionary view of the energy shock.

It increasingly looks like more market and economic pain—in both the US and Iran—will be needed to motivate a deal to reopen the Straits. However, with energy inventories rapidly falling, that tipping point will be a matter of weeks.

Solomonic solution

There is a hot debate about who holds the upper hand in the negotiations between the US an Iran. However, what matters to the current economic outlook is less about who “wins” than it is about how long it takes for a resolution and a reopening of the Straits.

Yesterday Trump wrote that “positive” discussions underway with Tehran “could lead to something very positive for all.” In addition, he wrote that the US would be guiding ships exiting the strait as “a Humanitarian gesture on behalf of the United States, Middle Eastern countries but, in particular, the Country of Iran.” Of course, there have been dozens of similarly optimistic claims since the start of the War nine weeks ago. Presumably, at some point this optimism will prove warranted, but why would that be now?

My reading of the reports around the war is that both sides have dug in for a long fight, and their positions are still miles apart. Consider the 14-point proposal from Iran last week. According to Iranian media it included:

· the withdrawal of US forces from areas surrounding Iran,

· lifting the US blockade on the strait of Hormuz,

· releasing Iran’s frozen assets,

· payment of compensation,

· lifting all sanctions,

· ending the war on all fronts, including Lebanon,

· and a new control mechanism for the Strait.

Missing was any suggestion that Iran was ready to end its nuclear program. Of course, that is a red line for the Trump Administration, but it seems to me that this proposal violates many red lines. I’m surprised the President didn’t declare it dead-on-arrival.

Again, based on press reports, both sides seem convinced that they have time on their side. On one side, the Trump Administration argues that a crippled military and a collapsing economy will force Iran to capitulate. On the other side, Iran thinks that a combination of rising inflation, weaker growth and declining approval ratings will force President Trump to capitulate.

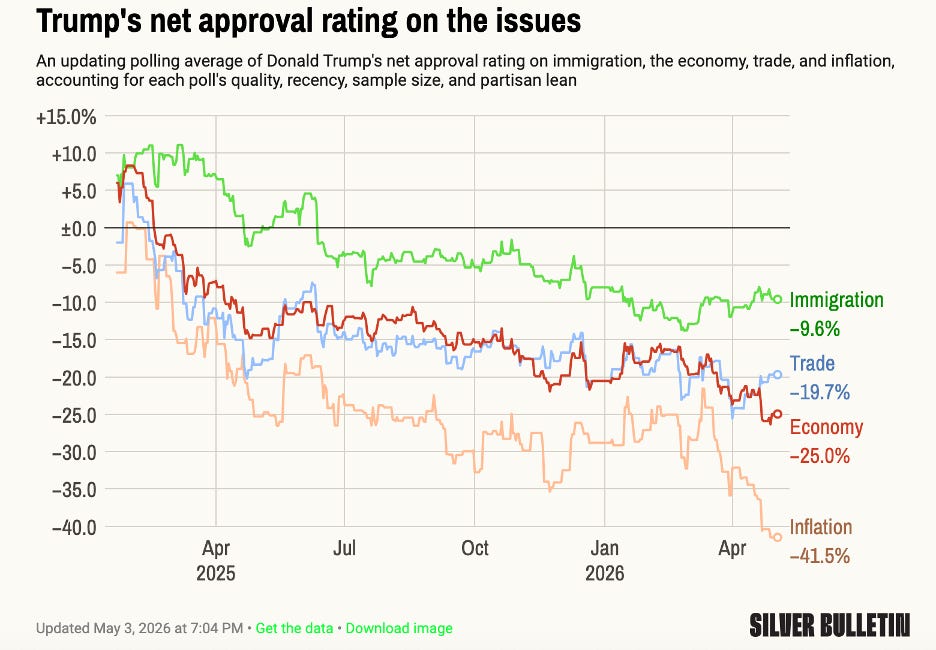

This suggests that it will take more pain to bring the two sides together. Trump’s approval ratings have been sliding steadily since the start of his second term (chart). The net disapproval around his trade and immigration policies have flattened out since those stories dropped out of the headlines in recent weeks. But his economic and inflation ratings continue to plunge. If he has held out so far, what level of disapproval would trigger a policy shift?

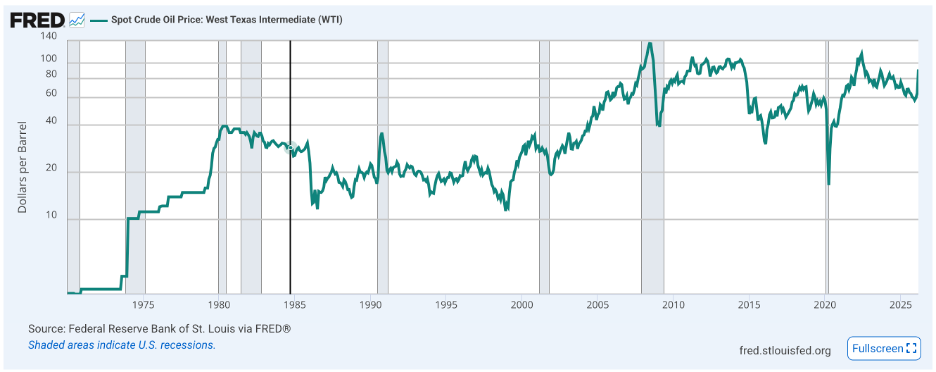

Meanwhile the rise in energy prices has been relatively modest by historic standards. After surging into the start of April, WTI seems to have settled in around $100/bbl and gasoline around $4/gal. This has allowed equity markets to focus on strong earnings. Trump’s favorite barometer, the equity market, is setting new records. The economy is also doing okay. Two out of three “pain markers” are fine. Why rush into a bad deal?

On the other side, it appears likely that the Iranian regime has been further radicalized. They have seen colleagues and family members killed and they have found a new tool for blackmailing the world—closing the Straits, using drones and missiles. The Iranian government has never seemed to care about how the general population is faring. I see an analogy with North Korea, which can do enough trade via land routes to take care of the elite, even as everyone else suffers. Iran seems to be in no rush to reach a deal either.

So far so good

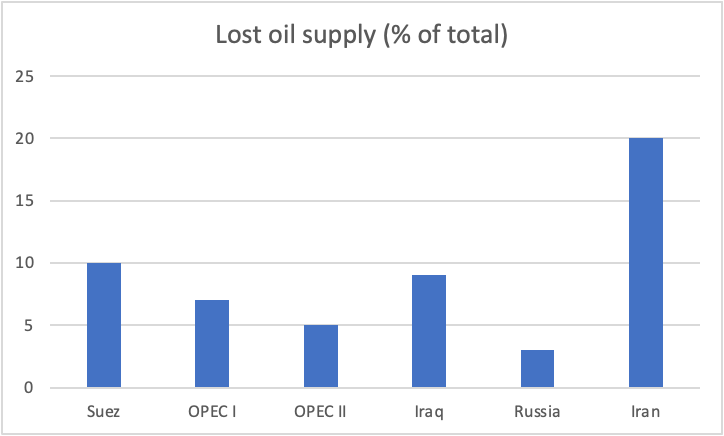

On a daily basis, this is by far the biggest shock ever to global energy supply. Almost 20% of global oil supplies have been blocked. That’s more than double any prior shock (chart). And yet, as the second chart shows (using a log scale), the percentage increase in the WTI oil price today is less than for previous supply disruptions. That muted price response is why the economic and market impacts have been relatively small so far.

Source: https://www.dallasfed.org/research/economics/2026/0320

An unstable “equilibrium”

This relatively benign outcome is clearly not sustainable, absent a near-term reopening of the Straits. At this point, since the shock is seen as mild and temporary, the three-step transmission to the economy is weak: (1) the rise in the price of oil is small, (2) much of that rise is absorbed by businesses that use oil in their products, and (3) consumers tend to keep spending. However, that transmission process is becoming a coiled spring. At some, point, as energy inventories steadily plunge: (1) crude prices will surge, (2) businesses will pass on a larger share of the cost to their consumers and (3) consumers will start treating the shock as a more permanent hit to real income. Adding insult to injury, the stock market will correct. A small shock to the economy will become a big shock.

As I’ve noted before the duration of the shock in some ways is more important than the size of the supply squeeze. A one-week disruption in 20% of global supply has virtually no impact on the economy. However, with every passing week the risk of a nonlinear response to the shock grows.

It is very hard to pin down when this nonlinear moment comes. It has been delayed due to both high initial inventories and optimism that an end to the shock is always just a few weeks away. I suggest that investors keep a close eye on “spot” prices for WTI oil, gasoline and other energy products. For several weeks in April energy prices seemed to have plateaued. However, in the last week or so prices have start to rise. For example, according to AAA, in the Week ending May 4th the average price of regular gas rose from $4.11/gal to $4.46/gal, marking one of the biggest weekly increases ever.

No pain, no gain

All of this leads to a rather depressing conclusion. I don’t expect a resolution without further pain. At some point, shortages of essential goods will grow so acute even the Iranian leaders fell the pain. As energy prices continue to rise, and the economy, markets and Presidential approval ratings sink, the US will also be more motivated for a deal. Along the way, I would not be surprised if the war heated up again, speeding up the price shock. Prepare for the worst, hope for the best.